Pitch

A temperature-indexed, revenue-neutral carbon tax reduces distortionary taxes, deficit, pollution, and the risks posed by climate change.

Description

Summary

A conservative’s model for pricing carbon provides tax and subsidy reform while addressing pollution in a fiscally and scientifically responsible manner.

The revenue-neutral carbon tax will start at $20/ton and will rise at 5% per annum in real terms indexed to global temperature change. The price index will remain fixed for 10 years at a time and will be updated every decade to reflect changes in global temperature. So if the few climate skeptics are correct and the world stops warming the price trends to $0. If the world starts warming at a more alarming rate the tax can ramp up accordingly. In this regard it is like a hedge, an insurance policy against future climate contingencies.

The elimination of ~$19 billion of energy subsidies per year will create a level playing field for the energy sector.

The revenue neutral component of the carbon tax will be achieved by cuts to capital gains taxes and corporate tax rates. 50% of the capital saved from eliminating subsidies will fund further corporate tax cuts reducing rates to 31%. 50% from subsidy reduction will be allocated towards deficit reduction.

1/7th of the carbon tax revenue is used for pension increases and income tax credits to the poorest households.

Border carbon adjustments ensure domestic exporters remain economically competitive and incentivizes action from other nations facing carbon tariffs.

A climate science communication program led by NASA will restore public confidence in the evidence for anthropogenic climate change and the need for action.

An independent review on the economics of climate change conducted by an expert advisory panel comprising mostly conservative specialists will convey the importance of pricing carbon to the public.

A carrot and stick negotiation process with dissenting congressmen could secure key support and necessary votes to pass legislation.

A pro carbon pricing business lobby consisting of leading business figures would counter misinformation from vested interest groups.

Category of the action

Mitigation - Helping U.S. enact carbon price legislation

What actions do you propose?

A carbon tax is a simple, transparent way to price greenhouse gas emissions. By placing a fixed, annually increasing price on carbon indexed to global temperatures, companies are able to factor this into future investment decisions.

The carbon tax will begin at $20/ton rising by 5% per annum in real terms indexed to global temperatures to adjust for changes in risk. As Hank Paulson notes on climate change - “Risk management is a conservative principle, as is preserving our natural environment for future generations.” Pertaining to this principle of risk management the former head of risk at Goldman Sachs, Dr Bob Litterman, notes that the most important principle in ExxonMobil's guide to climate risk is:

"· Adjust in the future to developments in climate science and the economic impacts of climate policies

(This) principle is perhaps the most important: the appropriate price for carbon emissions at each point in time should be determined by science and economics.”

Determining the appropriate price for carbon, a risk-based approach: According to the WMO temperatures rose 0.17 C in 1980, 0.14 C in 1990 and 0.21 in the 2000s (0.173 C/decade - see graph below). The global temperature indexation could be based on the average decadal change over the last two decades against the underlying average trend from 1980-2010. Deviations from the average 0.173 C/decade would alter the price of carbon. The underlying average trend could be updated after each decade. The index will remain fixed for a decade at a time. At the end of each decade the carbon tax would be re-calibrated, ensuring that business has certainty over the price of carbon for 10 years at a time. Periodic monitoring of climate models would allow businesses to forecast potential carbon prices for the following decade. The indexation model would be non-linear, meaning the further the two-decadal average deviates from the underlying mean, the greater the adjustment in price. This ensures that if global temperatures decrease, as some Republicans say they will, then the price can quickly trend to $0. If the climate begins to warm at unprecedented rates the carbon tax can quickly ramp up to meet increasing risks. A two-decadal average was chosen for comparison against the underlying mean because it provides a large enough sample to eliminate climate ‘noise’ such as aerosols, volcanoes, El Nino Southern Oscillation etc.

The exact methodology for determining and updating the non-linearity models for carbon price indexation will be informed by risk experts in conjunction with NASA. There is potential to adjust the linearity of the models every decade to reflect learning about the economic impacts of climate change. For example, if the associated economic impacts of a warmer world are lower than expected, the model’s linearity could be adjusted to increase price less as temperature rises diverge further upwards from the underlying mean.

Index pricing is often used for commodities such as oil-indexed LNG contracts. The formula for an indexed price is usually: CP = BP + β X

- BP: constant part or base price ($20/ton)

- β: gradient

- X: indexation (5%/annum real)

An S-curve contract price formula is different above and below a certain oil price, to dampen the impact of high volatility:

This temperature index, however, needs to increase non-linearly/decrease non-linearly when temperatures go outside certain bounds, so it differs slightly from a traditional indexed commodity. An example of how this index could operate: When the two-decadal average is ± 0.02 C from the underlying mean the carbon price index remains at 5%. For +0.02C to 0.05C the index rises at 0.50% per 0.01C and for -0.02C to -0.05C the index decreases at 0.50% per -0.01C. For each 0.01C increment higher than +0.05C the increase is (0.5%+ 0.1%*((x-0.05C)*100)) where x = deviation from underlying mean. For each 0.01C increment lower than -0.05C the decrease is (-0.5% - 0.1%*((x + 0.05C)*100)) where x = deviation from underlying mean. Click on the link below to see example:

Tax credit temperature derivatives could create a market in expected future tax rates (and thus temperatures) aiding business in pricing carbon for the future decade. The formation of this type of financial innovation would be left up to the private sector to create the appropriate financial tools for factoring the next decade's index into investment decisions.

Dr Bob Litterman, writing for the Cato Institute, recently stated, “The present value of damages is generally thought to be in a range of $5 to $35 per ton of carbon dioxide” meaning $20/ton is nicely in the middle of this range

Approximately 80% of the economy will be covered by the carbon tax with residential, commercial and agriculture sectors being exempt. The energy, transport and manufacturing sectors will face the cost of carbon. Covered gases will include carbon dioxide, methane (i.e. fugitive emissions from hydraulic fracturing) and synthetic gases (i.e. refrigerants). Facilities with under 25,000 tCO2-e per annum will be exempt from the carbon tax.

The total revenue from the carbon tax in the first year will be ~$105 billion. Commensurate with the carbon tax policy in British Columbia, approximately one seventh of revenue ($15 billion) would go towards alleviating regressivity through increased pensions and income tax credits. Of the remaining $90 billion, half will go towards capital gains tax (CGT) cuts which will reduce CGT from ~$80 billion per year (based on 2002-2006 average figures) to $35 billion per year. The other 50% will go towards corporate tax cuts from 35% to 31.5%.

{kind=link}

{kind=link}

The elimination of ~$19 billion of energy subsidies per year will create a level playing field for the energy sector ($1.5 billion in household energy efficiency subsidies would be retained to address market failures due to information asymmetries). States will be able to voluntarily provide continued support to renewable energy sectors through their own favored policy mechanisms. The phase out of subsidies may not be immediate, however, because it could cause sovereign risk as certain businesses may have made investment decisions based on the continuation of subsidies over the short-term. Once the subsidies have been fully phased out, expected to take 5 years, it will save $19 billion in annual expenditure. Half of this will go to deficit reduction, something which is of crucial importance for the United States. The other half will go towards corporate tax reductions, reducing the corporate tax rate further to ~31%. Deficit reduction payments and corporate tax reductions will be phased in gradually as energy subsidies are phased out to ensure fiscal responsibility.

Rationale for a capital gains tax reduction: A 2012 paper by Warwick McKibben, Adele Morris, Peter Wilcoxen and Yiyong Cai investigated an American carbon tax, with revenues used under the following scenarios:

1. Sequestered into the budget

2. Distributed as a dividend

3. Used to reduce labor taxes

4. Used to reduce capital gains taxes

Figure 26 within the paper illustrates that options 1, 2 and 3 produce negative economic impacts equivalent to a 4% decline in GDP output by 2030. Option 4, a reduction in capital gains taxes, conversely increases GDP by 2% by 2030. This means that, “in terms of GDP, then, the (CGT) swap appears to produce a double dividend, i.e. both emissions reductions and an increase in economic activity.” The finding that a CGT swap has the least impact on economic growth of revenue-neutral options is corroborated by a recent research paper by Resources for the Future. This is congruent with what most conservative economists have been saying all along – that a capital gains tax is duplicative and economically inefficient.

Rationale for a corporate tax reduction: At 35%, the United States has the highest nominal corporate tax rate in the developed world. This rate jumps to 39.2% when state taxes are taken into account. Despite this, the average effective federal tax rate was 12.6% in 2010. Currently US companies have ~$2 trillion in profits stockpiled overseas and tax inversion is common practice. Ron Wyden, the Oregon Democrat who chairs the Senate Finance Committee, recently stated, “it’s clear that America must establish a more efficient and competitive corporate tax rate”. Reducing the corporate tax rate to 31% will drive growth in entrepreneurship and innovation and will reduce the incentives for tax inversion.

Border carbon adjustments (BCAs) ensure domestic exporters remain economically competitive with businesses who operate in countries without a carbon price. BCAs will levy tariffs on imported goods not facing an equivalent carbon pricing impost. BCAs will also rebate exporters for carbon costs based on industry best practice benchmarking. In industry best practice benchmarking assistance will be provided to exporters based on the average carbon intensity of the most efficient 50% of the economy in that particular activity (similar to benchmarking used from phase III of the EU ETS). This incentivizes emissions reductions within activities towards industry best practice. It also ensures that the least efficient producers within an export sector are not compensated more than their carbon efficient competitors (as is the case with inequitable grandfathering of permits in cap-and-trade). It is important to implement BCAs based not only on scope 1 (direct) emissions, but also on scope 2 emissions (electricity pass-through costs). For example, energy intensive industries like aluminum would face a much higher cost impost via pass-through costs of electricity due to the carbon tax than via the carbon tax for their direct production emissions. This would also require tariffs on imports to be adjusted to include scope 1 and scope 2 emissions.

A climate science communication program led by NASA will restore public confidence in the evidence for anthropogenic climate change and the need for action. Despite 97% of climate scientists agreeing with the core tenets of anthropogenic climate change as outlined by the IPCC,many Americans do not believe in anthropogenic climate change. Existing funding would be re-allocated from other NASA projects negating the possibility of a congress blocking the initiative.

An independent review on the economics of climate change conducted by an expert advisory panel comprising academia, public sector and private sector specialists will convey the importance of pricing carbon to the public. This review will be similar to the Stern Review in the UK and the Garnaut Review in Australia, but will be represented by a panel as opposed to an individual. The panel will consist mainly of members from the conservative side of politics. The Republicans would fund this independent review. Examples of members that could be considered are:

· Hank Paulson

· William Nordhaus

· Bob Litterman

· Michael Bloomberg

· Bob Inglis

· Arthur Laffer

· Greg Mankiw

· Various climate science and risk experts to assist in determining the temperature indexation model.

A carrot and stick negotiation process with dissenting congressmen and senators could secure key support and necessary votes to pass legislation. There are a number of options available:

Carrots:

· Increase the liberalization of the gas market by allowing more export liquefied natural gas (LNG) facilities to be built. This would be good economically and could also ease energy security problems faced by the Ukraine and the EU.

· Decrease and/or remove inefficient EPA regulations associated with reducing carbon emissions if a national carbon tax is passed, with the caveat that these regulations will come back into effect if the legislation is repealed.

· Economic support plans for the most affected states may also be brokered to ensure a smooth transition for the new policy.

Sticks:

· Propose stricter regulations to reduce greenhouse gas emissions.

Who will take these actions?

The actors will be the current Republican party. It will be pushed as the party line of the Republicans for the next election. In a personal discussion I had with NASA political and science historian Dr Erik Conway in 2010 he told me that it is only the Republicans who will be able to enact a federal price on carbon.

Republicans have a strong history in supporting the environment with President Nixon enacting the Clean Air Act in 1970. Even very conservative Republicans like Rick Perry have supported strong pollution reduction measures, albeit SOX and NOX, at state level. Proposing this at the next election would provide much needed votes from the younger demographic and more environmentally concerned, fiscally conservative individuals.

The Republicans will need to be pushed by lobbyists. Climate Colab can organize meetings with influential Republicans to propose this idea. The first step will be convincing the Republican party to commission the independent review of the economics of climate change.

NASA would start its nation-wide campaign on improving climate science literacy once the Republicans are in power. This messaging on the need to act on climate change (NASA) and the ways in which to respond to climate change (review panel) will provide clear messaging to the public.

A pro carbon pricing business lobby consisting of leading business figures such as Bill Gates, Rex Tillerson, Warren Buffett and Tim Cook would provide the required voice from the private sector. The establishment of this business group would need to be done by Climate Colab or other climate NGOs.

Negotiations with dissenting senators and congressmen, via the aforementioned carrot and stick approach, will allow for necessary concessions.

Once the bill is passed the EPA would implement the carbon tax. NASA and a panel of expert risk individuals would manage the global temperature indexation model.

Where will these actions be taken?

The carbon tax and energy subsidy reform package will be brought forward to the house by the Republicans, will be legislated in congress and will be implemented nationally. This should catlayse action in many other nations, including China, Brazil, Mexico, South Africa, India and Australia. Strong border carbon adjustments provide further incentives for other nations to act in accordance with the United States. This proposal could be taken to the UN Conference of Parties for UNFCCC negotiations and the US could seek feedback from other nations and could propose similar measures for major trading partners. It is likely that the proposal would get very strong praise and support from the international community which would strengthen the American people’s perception of the policy. The reason for this is that America cannot afford to act unilaterally on climate change and expect other nations to simply follow suit. A consultative process, similar to Ronald Reagan’s described by George Shultz in the Climate Colab webinar, is needed with major polluting countries to ensure a global agreement.

NASA’s improving climate change science literacy program would be rolled out nationally. It would be rolled out in primary, secondary and tertiary education centers and targeted appropriately. NASA would also deliver messages on social media and through radio and television interviews.

The wonderful thing about a carbon price is that it is hard to say definitively where and how emissions will be reduced. The market and free enterprise can solve the problem through innovation and entrepreneurship.

How much will emissions be reduced or sequestered vs. business as usual levels?

According to the CBO a carbon tax starting at $20 per ton would cut U.S. emissions an extra 8 percent by 2021. This would get the United States in range of its Copenhagen pledge to cut emissions 17 percent by 2020.

The price on pollution would also help ensure the US meets its likely Paris target of 33% below 2005 levels by 2030. Revision of the carbon price once per decade via the temperature indexation model would ensure that the carbon tax remains proportionate to the risk posed. Hence targets may need to be increased or decreased. A good aspect of temperature indexation is that long-term required projections (such as an 83% target by 2050) become less relevant over the short-term, as it is known the target will automatically adjust by an approach which is commensurate with risk.

The emissions would continue to decline in order to meet the nation's target of 83% below 2005 levels by 2050, however this target is subject to revision from the global temperature indexation model.

What are other key benefits?

Broader corporate tax reform is essential for reducing tax inversion, promoting enterprise, increasing economic growth and aiding in the structural transformation towards an efficient services-based economy.

Deficit reduction of ~$9.5 billion per annum via subsidy reform will provide a much needed wedge towards reducing the burgeoning debt-to-gdp ratio.

It is estimated that total energy consumption in the US was 97,534 billion BTUs in 2013. America also accounts for approximately ¼ of the world’s annual oil consumption. The American Council for an Energy-Efficient Economy recently found that America wastes a “tremendous” amount of energy and many opportunities for efficiency gains were present. A price on carbon will drive efficiencies in the use of fossil fuels allowing:

· Greater energy security. Lower cost of securing oil reserves in the Middle East.

· Reduced respiratory disease will result from lower emissions of particulate matter, SOX and NOX. An IMF study finding:

What are the proposal’s costs?

In assessing the economic impacts of this structural tax reform it is useful to compare the performance of other economies with similar policies to investigate the potential outcomes for the United States:

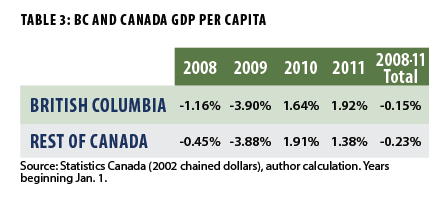

British Columbia: Due to its revenue-neutrality via both income tax cuts and corporate tax cuts, British Columbia’s carbon tax is the most similar policy to the one proposed. BC’s levy started at C$10 ($9) a ton in 2008 and rose by C$5 each year until it reached C$30 per ton in 2012. Through revenue-neutrality BC now has the lowest personal income tax rate in Canada and one of the lowest corporate rates in North America.

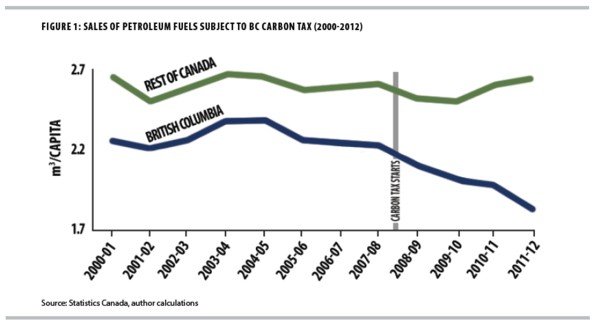

BC’s fuel consumption is also down. Over the past six years, the per-person consumption of fuels has dropped by 16%. During that same period, per-person consumption in the rest of Canada rose by 3%. Since implementation BC’s economy has grown at a faster rate than the average of the rest of the Canadian economy.

Sweden: The carbon tax in Sweden began at $100 per ton in 1991 and increased to $150 per ton in 1997. Economic growth is in line with long-term trends. Between 1990 and 2006, Sweden's economy grew by 44-46 percent (approx 2.8% annually).

Norway: A carbon tax on gasoline began in 1991 and has been levied at an average rate of $21 per ton. Norway’s economic output appears unaffected with nominal per capita incomes reaching $101,000 in 2013.

Australia: A carbon tax beginning at $23 resulted in a 0.8% reduction in emissions in the first calendar year (the highest calendar year reduction in 24 years). Treasury estimates the economic impacts to be less than 0.1% of annual GDP.

The following graph illustrates that green taxes in various European countries have actually provided net benefits to GDP:

The applicability of these findings to the US economy is uncertain. The economic review of climate change should elucidate this more.

Some carbon intensive energy would likely face asset value write downs if a carbon tax legislation were to be passed.

Time line

The carbon tax will be the primary mechanism for achieving the nation’s 2020 targets of 17% below 2005 levels by 2020, 33% below 2005 levels by 2030 and 83% below 2005 levels by 2050 subject to revision by the temperature indexation model.

Short-term:

· Establish the panel for the review of the economics of climate change in early 2015 and begin the review.

· Begin drafting a new bill for the carbon tax, but leave it open to change following the review’s recommendations.

· Receive feedback from the review of the economics of climate change in Q3 2015.

· Roll out the communication program on the economic benefits of the tax and subsidy reform.

· Provide the Republicans formal response to the review in Q4 2015.

· Finalize the carbon tax bill by the end of 2015 ready for the 2016 presidential election.

· Release a high-level explanatory memorandum so that the media and the market can easily digest the proposal.

· Release a white paper in Q1 2016 for feedback from industry, business, academia and individuals on the proposed bill.

· Receive submissions to the white paper and formalize a response in Q2 2016.

· Update legislation to accommodate important feedback received during the white paper process. Release the updated bill to the lower house in 2016 regardless of whether the Republicans win the election,

· Legislate in 2016 for implementation in 2017.

· Roll out NASA’s improving climate change science literacy program in late 2016 if the Republicans win the election.

· The US will continue to work with other nations to provide capacity building for implementing similar programs. This would be similar to the World Bank’s Partnership for Market Readiness program.

Medium-term

· Continue the global temperature indexation model.

· The US will continue to work with other nations to provide capacity building for implementing similar programs.

Long-term

· Continue global temperature indexation.

Related proposals

The carbon tax would be the cornerstone of actions to mitigate climate change in the US.

The carbon tax would be the cornerstone of emissions reductions in industry.

Substantial action on climate change by the US is key to unlocking greater action from other nations. The carbon tax in America will likely catalyze similar actions in other nations due to BCAs.

A carbon tax will be the cornerstone policy to reduce emissions in the US energy sector.

A carbon tax will be part of the policy suite to reduce emissions in the US transport sector.

A carbon tax sends a strong price signal to buildings which are energy inefficient and carbon intensive.

References

Public opinion on climate change vs scientific opinion on climate change:

Expert credibility in climate change, (Anderegg et al, 2010)

Examining the scientific consensus on climate change, (Doran, 2009)

The Economics of Pricing Carbon:

Stern Review: The economics of climate change, (Stern, 2006)

Garnaut Climate Change Review, (Garnaut, 2011)

A Review of the Stern Review on the Economics of Climate Change, (Nordhaus, 2007)

What is the right price for carbon emissions?, (Litterman, 2013), Paper for the Cato Institute. (probably the best article on this topic I have read)

Pricing carbon when we don't know the right price, (Pindyck, 2013), Paper for the Cato Institute.

Carbon tax

Europe’s experience with carbon-energy taxation, (Mikael Skou Andersen, 2010)

Carbon taxes and corporate reform, (Donald Marron and Eric Toder, 2013), The Urban Institute and Urban-Brookings Tax Policy Center.

Climate change policy's interactions with the tax system, Lawrence Goulder, 2013)

Effects of US tax policy on greenhouse gas emissions, Committee on the Effects of Provisions in the Internal Revenue Code on Greenhouse Gas Emissions Board on Science, Technology, and Economic Policy Policy and Global Affairs (William D. Nordhaus, Editor Stephen A. Merrill, Editor Paul T. Beaton, Editor, 2013)

The potential role of a carbon tax in US fiscal tax reform, (McKibben, Morris, Wilcoxen and Cai, 2012)

Getting Energy Prices Right : From Principle to Practice, (Ian Parry, Dirk Heine, Eliza Lis, Shanjun Li, International Monetary Fund, July 2014)

Regressivity - Distributional impacts of pricing carbon using a CGT swap

The Initial Incidence of a Carbon Tax across Income Groups, (Robert C. Williams III, Hal Gordon, Dallas Burt raw , Jared C. Carbone, and Richard D. Morgenstern). Considering a Carbon Tax: A Publication Series from Resources for the Future’s Center for Climate and Electricity Policy (August 2014)

Tax Reform

The High Burden of State and Federal Capital Gains Taxes, February 20, 2013, By Kyle Pomerlau, Tax Foundation

Climate Risk

The price of climate risk, (Bob Litterman, 2013)

Tail risk and the price of carbon emissions, (Bob Litterman, 2012)